A sales manager has analysed a sample of 350 sales transactions from the latest period. The manager wishes to investigate:

how many customers made their purchase online using the internet and how many purchased by telephone.

how many were new customers and how many were placing repeat orders.

The following table shows the results of the analysis.

If the pattern of sales occurs next period, the probability of a particular sale being a repeat order placed online is closest to:

The staffing policy for a supermarket is to have one cashier station open for every forecasted 20 customers per hour. Cashiers are hired by the hour as and when required, and do not perform any other duties.

The cost of the cashiers in relation to the number of customers would be classified as which type of cost?

Which of the following statements regarding variances is valid?

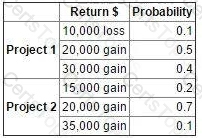

The possible returns and associated probabilities of two independent projects are as follows:

It has been decided that both projects are to be launched.

Which TWO of the following statements are correct? (Choose two.)

Which of the following would NOT be an appropriate performance measure for a profit centre manager?

The International Federation of Accountants (IFAC) stated that it was important that “accountants in business” should understand what the drivers of stakeholder value are. Which of the following statements is valid?

Which TWO of the following are characteristics of Management Accounts? (Choose two.)

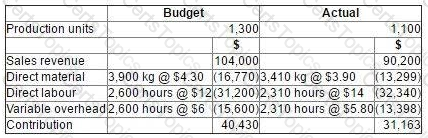

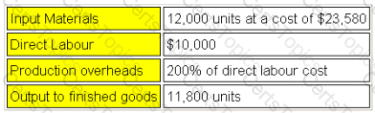

Data for the latest period for a company which makes and sells a single product are as follows:

There were no budgeted or actual changes in inventories during the period.

The variable overhead expenditure variance for the period was:

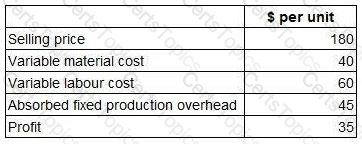

A company makes and sells a range of products. The standard details per unit for one of these products, product X, are as follows.

To meet sales demand, the company must obtain 2,000 units of product X next month. There is sufficient labour capacity to produce 1,500 of these units in-house during normal time. However, any production above this level would require overtime working which would be paid at a premium of 50%.

The company can buy as many units of product X as it wishes next month from an external supplier at a price of $120 per unit.

What is the total financial benefit to the company of purchasing the appropriate number of units from the external supplier rather than producing them in-house?

The records of a manufacturing company show the following relationship between total cost and output.

The budgeted output for Period 3 is 27,000 units. Assume that previous cost behaviour patterns will continue.

What is the total budgeted cost for Period 3?

Give your answer in the nearest whole number.

Which THREE of the following are parts of the master budget? (Choose three.)

A company operates an integrated standard cost accounting system. The standard price of raw material A is $20 per litre. At the start of period 1, the inventory of 500 litres of raw material A was valued at $20 per litre. During period 1, 100 litres of raw material A were purchased at an actual price of $21 per litre. During period 2, 550 litres of raw material A were issued to Job 789.

In respect of the above events, which TWO of the following statements are correct? (Choose two.)

Which of the following is a relevant cost?

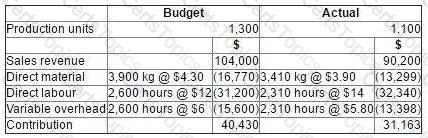

Data for the latest period for a company which makes and sells a single product are as follows:

There were no budgeted or actual changes in inventories during the period.

The sales volume contribution variance for the period was:

The forecast costs per unit for a new product are as follows:

The company uses marginal cost plus pricing and all products are required to achieve a 40% margin.

What would be the selling price per unit?

The following data are available for a company that produces and sells a single product.

The company’s opening finished goods inventory was 2,500 units.

The fixed overhead absorption rate is $8.00 per unit.

The profit calculated using marginal costing is $16,000.

The profit calculated using absorption costing and valuing its inventory at standard cost is $22,400.

The company’s closing finished goods inventory is:

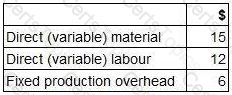

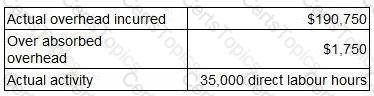

A company absorbs production overhead using a direct labour hour rate. Data for the latest period are as follows:

What is the overhead absorption rate per direct labour hour? Give your answer to one decimal place.

A new product requires an investment of $200,000 in machinery and working capital. The total sales volume over the product’s life will be 5,000 units. The forecast costs per unit throughout the product’s life are as follows:

The product is required to earn a return on investment of 35%.

What unit selling price needs to be achieved?

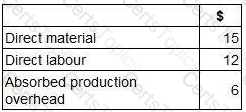

A company uses standard absorption costing. Budgeted and actual data for the latest period are as follows.

What was the production overhead absorption rate per unit?

Refer to the Exhibit.

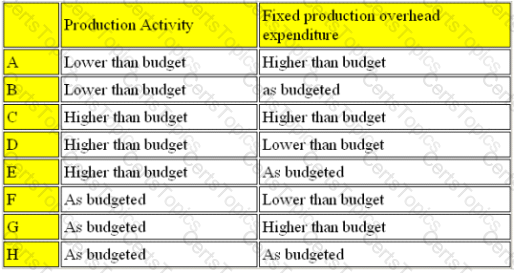

A company operates an absorption costing system. The management accounts show that fixed production overheads were over-absorbed in the period.

Which FOUR combinations could possibly have resulted in this situation?

Refer to the exhibit.

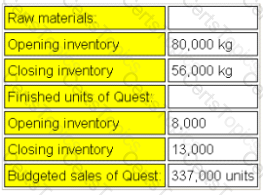

Data for October's budget for product Quest for the month of October are given below:

Each unit of Quest requires 6kg of raw materials. Strict quality control procedures are applied to the manufacturing process and normal rejection levels are 5% of finished units.

The raw materials purchases budget for the month of October is:

A product sells for £10 per unit and has an annual break-even volume of 50,000 units. The annual fixed costs are £100,000.

The variable cost per unit is:

Give your answer to 2 decimal places.

A company’s cash budgetary plans show that there will be surplus cash for three months of the forthcoming year.

Which THREE of the following would be appropriate management actions in this situation?

The materials price variance will be adverse when:

A company uses an integrated accounting system.

The accounting entries for the sale of goods on credit would bE.

Each unit of product GM requires 4 labour hours to be produced. 25% of the units will be completed during overtime hours.

Sales of 24,000 units are planned and finished goods inventory is budgeted to rise by 2,000 units.

If the wage rate is £6 per hour and the overtime premium is 50%, what is the budgeted labour cost?

Refer to the exhibit.

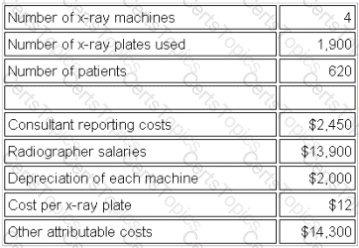

The following data are available for last period for the x-ray department of a local hospital:

The x-ray department cost per patient for last period was (to the nearest $0.01) is:

Which of the following categories of costs is the most relevant for decision making?

Which one of the following is a characteristic of strategic financial information?

Refer to the Exhibit.

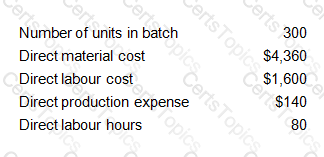

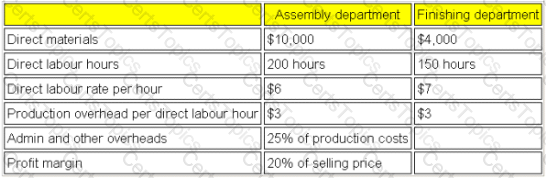

A company operates a batch costing system.

Production overhead costs are absorbed into the cost of batches using a direct labour hour rate. Other overhead costs are absorbed at a rate of 20% of total production cost. The company adds a mark-up of 10% to total cost in order to derive its selling prices.

Budgeted production overheads for the period are $44,000 and the budgeted level of activity is 8,800 direct labour hours.

The following data are available for batch number 309:

The required selling price per unit (to two decimal places) is:

Refer to the exhibit.

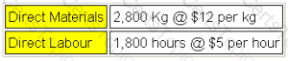

The following information relates to Job 123:

The selling price to the customer for Job 123 is:

Which of the following is the LEAST appropriate basis on which to apportion the insurance costs of plant and machinery:

A company operates an absorption costing system. Overheads are absorbed using a pre-determined absorption rate using labour hours.

Actual labour hours were 10% below budget for the period and overheads incurred were 10% above budget for the period. This would result in:

Refer to the exhibit.

T operates a process costing system. Data is available for Process A for the month of July.

Inputs for the month:

Normal losses are 15% of input and can be sold for $6 per kg. Actual output was 2,600 kg. There is no opening or closing work in progress for the period.

What is the value of the output from the process in the month?

In a company's sales ledger department, one additional invoice clerk is needed for every eighty customers added to the customer database. The total salary cost of invoice clerks is best described as:

In investment appraisal, the internal rate of return is

Refer to the exhibit.

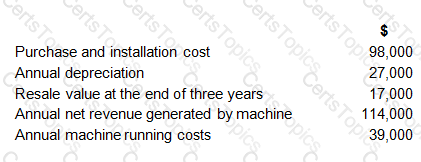

A company is considering purchasing a machine that will have a useful life of three years after which time it will be sold. Relevant cash flows relating to the purchase and operation of the machine are as follows.

The annual cost of capital is 14%.

The net present value of the investment in the machine is, to the nearest whole $:

Refer to the exhibit.

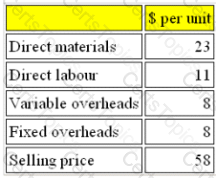

SL manufactures a single product, the cost and selling price of which are given below:

Fixed overheads per unit are based on a budgeted production volume of 25,000 units.

Budgeted sales are assumed to be 25,000 units.

If all costs increase by 5% but selling price remains the same, by how much must sales change from the budgeted volume to achieve the same budgeted profit?

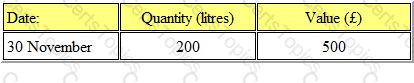

Refer to the Exhibit.

Fabex Ltd manufactures a household detergent called "Clear". The standard data for one of the chemicals used in production (chemical XTC) is as follows:

(a) 50 litres used per 100 litres of 'Clear' produced

(b) Budgeted monthly production is 1000 litres of 'Clear'.

The closing inventory of chemical XTC for November valued at standard price was as follows:

Actual results for the period during December were as follows:

(a) 500 litres of chemical XTC was purchased for £1300.

(b) 550 litres of chemical XTC was used.

(c) 900 litres of 'Clear' was produced.

It is company policy to extract the material price variance at the time of purchase.

What is the total direct material price variance (to the nearest whole number)?

Which one of the global principles of management accounting should be tailored to the knowledge of the decision maker?

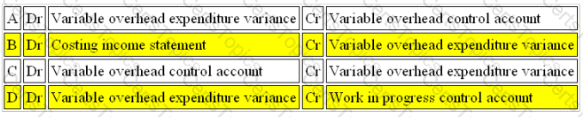

Refer to the exhibit.

Which is the correct journal entry required to record a favorable variable overhead expenditure variance in an integrated accounting system?

The correct journal entry required to record a favorable variable overhead expenditure variance in an integrated accounting system is:

In investment appraisal, the net present value (NPV) is

Xter Ltd produces product 'PZ'. The forecast sales for the forthcoming year are 50,000 units.

It is anticipated that there will be 10,000 units of opening inventory at the beginning of the year. However, management wishes to reduce this inventory by 30% by the end of next year.

The production budget for the forthcoming year will be

Refer to the exhibit.

PD manufactures a product in a process operation. Normal loss is 5% of input and occurs at the end of the process. The following data is available for the month of August:

What was full cost of output to finished goods in August?

Which THREE of the following statements could explain why a favourable sales volume contribution variance has arisen?

A company hires a delivery vehicle for $200 per day plus $2 per kilometre travelled. The total hire cost would be described as:

Which of the following statements is correct?

(i) Public sector bodies use annual budgets and thus have no need for longer term strategic planning information

(ii) Public sector budgets are fixed budgets therefore the use of flexible budgets for cost control purposes is not appropriate

(iii) Public sector performance indicators include both financial and non-financial information

Which one of the following is an advantage of business partnering roles for the management accounting function within an organisation?

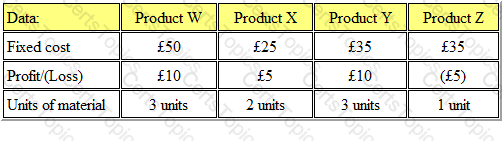

Refer to the exhibit.

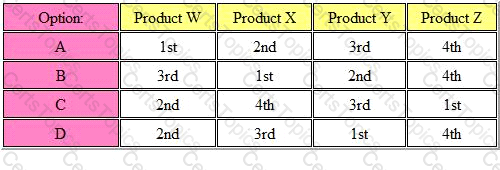

SS Ltd. manufactures four products which require the same type of material. The following fixed cost and profit/(loss) per unit is available:

In a period in which materials are in short supply, which of the following options is the rank order of production?

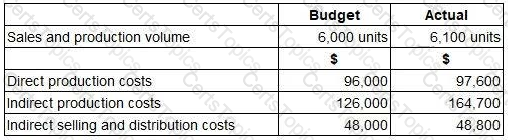

During the first financial period of this year a company posted profit of £340,000. However, their overheads were over absorbed by £20,000 in this period. As a result they tried to update their absorption rate for the current

period and as such they ended up under absorbing their overheads by £12,000.

They have also reported a sales volume increase of 550 when comparing this period to last.

You have been given the following information on unit cost/prices:

Selling price = £95 per unit

Variable production cost per unit = £15

Variable selling cost per unit = £18

Fixed overhead per unit = £8

They have asked you to reconcile their profit between periods.

Based on the information you have been given, what is their profit for the current period?

In process costing, the term equivalent units refers to :

Over absorption of overhead will always arise when:

Refer to the exhibit

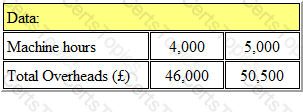

Zeff Ltd has forecast that the relationship between total overheads and machine hours will be as follows:

If the budget is to be based on 4,000 machine hours, the fixed overhead absorption rate will be:

Give your answer to 2 decimal places.

Refer to the exhibit.

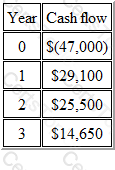

A project is forecast to generate the following cash flows.

Using three decimal places in all discount factors, the net present value (NPV) for the project at a cost of capital of 14.5% is (to the nearest $)

Which of the following would have an impact on the cash budget?

(a) Change in payables terms

(b) Change in the rate of depreciation

(c) Change in the percentage discount allowed

(d) Change of inventory holding policy

In investment appraisal, the calculation of the payback period

Refer to the exhibit.

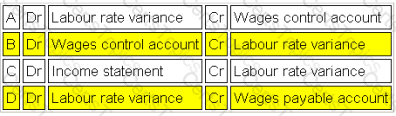

Which is the correct journal entry required to record an adverse labour rate variance in an integrated accounting system?

The correct journal entry required to record an adverse labour rate variance in an integrated accounting system is:

Copyright © 2021-2026 CertsTopics. All Rights Reserved