For a given notional amount, which of the following carries the greatest counterparty exposure (assuming the same counterparty credit rating for each):

Loss from a lawsuit from an employee due to physical harm caused while at work is categorized per Basel II as:

Which of the following is the most important problem to solve for fitting a severity distribution for operational risk capital:

Credit exposure for derivatives is measured using

Which of the following contributed to the systemic failure during the credit crisis that began in 2007?

Identify the correct sequence of events as it unfolded in the credit crisis beginning 2007:

I. Mortgage defaults increased

II. Collapse in prices of unrelated assets as banks tried to create liquidity

III. Banks refused to lend or transact with each other

IV. Asset prices for CDOs collapsed

A risk analyst attempting to model the tail of a loss distribution using EVT divides the available dataset into blocks of data, and picks the maximum of each block as a data point to consider.

Which approach is the risk analyst using?

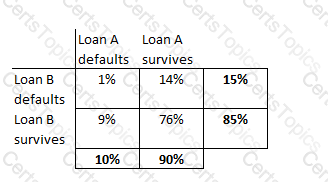

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. Theprobability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

Which of the following are valid approaches to leveraging external loss data for modeling operational risks:

I. Both internal and external losses can be fitted with distributions,and a weighted average approach using these distributions is relied upon for capital calculations.

II. External loss data is used to inform scenario modeling.

III. External loss data is combined with internal loss data points, and distributions fitted to the combined data set.

IV. External loss data is used to replace internal loss data points to create a higher quality data set to fit distributions.

An investor enters into a 5-year total return swap with Bank A, with the investor paying a fixed rate of 6% annually on a notional value of $100m to the bank and receiving thereturns of the S&P500 index with an identical notional value. The swap is reset monthly, ie the payments are exchanged monthly. On Jan 1 of the fourth year, after settling the last month's payments, the bank enters bankruptcy. What is the legal claim thatthe hedge fund has against the bank in the bankruptcy court?

The loss severity distribution for operational risk loss events is generally modeled by which of the following distributions:

I. the lognormal distribution

II. The gamma density function

III. Generalized hyperbolic distributions

IV. Lognormal mixtures

Which of the following statements is true:

I. Expected credit losses are charged to the unit's P&L while unexpected losses hit risk capital reserves.

II. Credit portfolio loss distributions are symmetrical

III. For a bank holding $10m in face of a defaulted debt that it acquired for $2m, the bank's legal claim in the bankruptcy court will be $10m.

IV. Thelegal claim in bankruptcy court for an over the counter derivatives contract will be the notional value of the contract.

Which of the following represents a riskier exposure for a bank: A LIBOR based loan, or an Overnight Indexed Swap? Which of the two rates is expected to be higher?

Assume the same counterparty and the same notional.

If A and B be two debt securities, which of the following is true?

Which of the following is not an event of default covered in the ISDA Master Agreement?

I. failure to pay or deliver

II. credit support default

III. merger without assumption

IV. Bankruptcy

Which of the following statements is true:

I. Confidence levels for economic capital calculations are driven by desired credit ratings

II. Loss distributions for operational risk are affected more by theseverity distribution than the frequency distribution

III. The Advanced Measurement Approach (AMA) referred to in the Basel II standard is a type of a Loss Distribution Approach (LDA)

IV. The loss distribution for operational risk under the LDA (Loss Distribution Approach) is estimated by separately estimating the frequency and severity distributions.

There are three bonds in a diversified bond portfolio, whose default probabilities are independent of each other and equal to 1%, 2% and 3% respectively over a 1 year time horizon. Calculate the probability that exactly 1 of the three bonds will default.

Which of the following is not a parameter to be determined by the risk manager that affects the level of economic credit capital:

Company A issues bonds with a face value of$100m, sold at $98. Bank B holds $10m in face of these bonds acquired at a price of $70. Company A then defaults, and the recovery rate is expected to be 30%. What is Bank B's loss?

Pick underlying risk factors for a position in an equity index option:

I. Spot value for the index

II. Risk free interest rate

III. Volatility of the underlying

IV. Strike price for the option

If X represents a matrix with ratings transition probabilities for one year, the transition probabilities for 3 years are given by the matrix:

Under the standardized approach to determining operational risk capital, operations risk capital is equal to:

Which loss event type is the failure to timely deliver collateral classified as under the Basel II framework?

CreditRisk+, the actuarial model for calculating portfolio credit risk, is based upon:

Whichof the following statements are true in relation to Historical Simulation VaR?

I. Historical Simulation VaR assumes returns are normally distributed but have fat tails

II. It uses full revaluation, as opposed to delta or delta-gamma approximations

III. Acorrelation matrix is constructed using historical scenarios

IV. It particularly suits new products that may not have a long time series of historical data available

Which of the following statements are true:

I. Credit VaR often assumes a one year time horizon, as opposed to a shorter time horizon for market risk as credit activities generally span alonger time period.

II. Credit losses in the banking book should be assessed on the basis of mark-to-market mode as opposed to the default-only mode.

III. The confidence level used in the calculation of credit capital is high when the objective is tomaintain a high credit rating for the institution.

IV. Credit capital calculations for securities with liquid markets and held for proprietary positions should be based on marking positions to market.

Which of the following is not a tool available to financial institutions for managing credit risk:

If the marginal probabilities of default for a corporate bond for years 1, 2 and 3 are 2%, 3% and 4% respectively, what is the cumulative probability of default at the end of year 3?

An error by a third party service provider results in a loss to a client that the bank has to make up. Such as loss would be categorized per Basel IIoperational risk categories as:

Which of the following statements are true?

I. Retail Risk Based Pricing involves using borrower specific data to arrive at both credit adjudication and pricing decisions

II. An integrated 'Risk Information Management Environment' includes two elements - people and processes

III. A Logical Data Model (LDM) lays down the relationships between data elements that an organization stores

IV. Reference Data and Metadata refer to the same thing

Which of the following decisions need to be made as part of laying down a system for calculating VaR:

I. The confidence level and horizon

II. Whether portfolio valuation is based upon a delta-gamma approximation or a full revaluation

III. Whether the VaR is to be disclosed in the quarterly financial statements

IV. Whether a 10 day VaR will be calculated based on 10-day return periods, or for 1-day and scaled to 10 days

Which of the following techniques is used to generate multivariate normal random numbers that are correlated?

Which of the following credit risk models considers debt as including a put option on the firm's assets toassess credit risk?

Which of the following is the best description of the spread premium puzzle:

A financial institution is considering shedding a business unit to reduce its economic capital requirements. Which of the following is an appropriate measure of theresulting reduction in capital requirements?

The sensitivity (delta) of a portfolio to a single point move in the value of the S&P500 is $100. If the current level of the S&P500 is 2000, and has a one day volatility of 1%, what is the value-at-risk for this portfolio at the 99% confidence and a horizon of 10 days? What is this method of calculating VaR called?

Copyright © 2021-2026 CertsTopics. All Rights Reserved