Which of the following contributed to the systemic failure during the credit crisis that began in 2007?

Identify the correct sequence of events as it unfolded in the credit crisis beginning 2007:

I. Mortgage defaults increased

II. Collapse in prices of unrelated assets as banks tried to create liquidity

III. Banks refused to lend or transact with each other

IV. Asset prices for CDOs collapsed

A risk analyst attempting to model the tail of a loss distribution using EVT divides the available dataset into blocks of data, and picks the maximum of each block as a data point to consider.

Which approach is the risk analyst using?

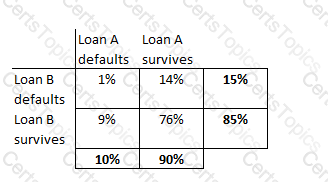

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. Theprobability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

Copyright © 2021-2026 CertsTopics. All Rights Reserved