Determine the price of a 3 year bond paying a 5% coupon. The 1,2 and 3 year spot rates are 5%, 6% and 7% respectively. Assume a face value of $100.

Which of the following is NOT a historical event which serves as an example of a short squeeze that happened in the markets?

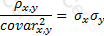

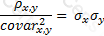

The relationship between covariance and correlation for two assets x and y is expressed by which of the following equations (where covarx,y is the covariance between x and y, σx and σy are the respective standard deviations and ρx,y is the correlation between x and y):

A)

B)

C)

D)

None of the above

Consider a portfolio with a large number of uncorrelated assets, each carrying an equal weight in the portfolio. Which of the following statements accurately describes the volatility of the portfolio?

Copyright © 2021-2026 CertsTopics. All Rights Reserved