Which of the following is not a credit event under ISDA definitions?

When building a operational loss distribution by combining a loss frequency distribution and a loss severity distribution, it is assumed that:

I. The severity of losses is conditional upon the number of loss events

II. The frequency of losses is independent from the severity of the losses

III. Both the frequency and severity of loss events are dependent upon the state of internal controls in the bank

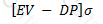

If EV be the expected value of a firm's assets in a year, and DP be the 'default point' per the KMV approach to credit risk, and σ be the standard deviation of future asset returns, then the distance-to-default is given by:

A)

B)

C)

D)

A statement in the annual report of a bank states that the 10-day VaR at the 95% level of confidence at the end of the year is $253m. Which of the following is true:

I. The maximum loss that the bank is exposed to over a 10-day period is $253m.

II. There is a 5% probability that the bank's losses will not exceed $253m

III. The maximum loss in value that is expected to be equaled or exceeded only 5% of the time is $253m

IV. The bank's regulatory capital assets are equal to $253m

Copyright © 2021-2026 CertsTopics. All Rights Reserved